The global financial landscape is undergoing a fundamental transformation as digital currencies challenge centuries-old monetary systems. Understanding the distinct advantages of cryptocurrency versus traditional fiat money has become essential for anyone navigating today’s economy—whether you’re an investor, business owner, or simply a financially curious individual.

This comprehensive analysis examines the unique benefits each monetary system offers, backed by current data, expert perspectives, and practical insights to help you make informed decisions about how these currencies fit into your financial strategy.

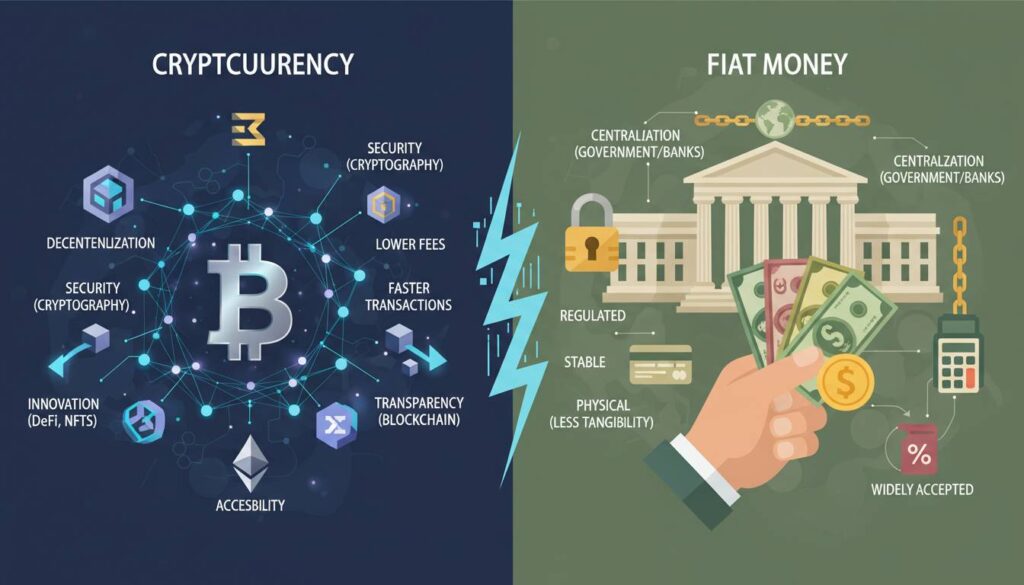

Understanding the Fundamental Differences

Before exploring advantages, it’s crucial to establish what distinguishes these two monetary systems. Fiat money—derived from the Latin word “fiat” meaning “let it be done”—refers to government-issued currency that operates without intrinsic value and is not backed by physical commodities like gold. The U.S. dollar, euro, yen, and British pound all represent fiat currencies, deriving their value primarily from governmental regulation and public trust in the issuing authority.

🌍 From Fiat to PiCoin – The Revolution in Global Payments

1. Traditional Money Transfer Mechanism (Fiat)

For hundreds of years, the global financial system has mainly operated on fiat money and intermediary banks. The process of sending money from one person to another… pic.twitter.com/4YMhDZuAFZ

— Learn everything (@dannamviet) September 8, 2025

Cryptocurrency, conversely, operates on decentralized networks using blockchain technology—a distributed ledger system that records transactions across multiple computers in a way that makes the records extremely difficult to alter retroactively. Bitcoin, introduced in 2009, pioneered this approach, creating a peer-to-peer electronic cash system that eliminates the need for intermediaries like banks.

The fundamental philosophical difference lies in centralization versus decentralization. Fiat currencies derive authority from central banks and governments, while cryptocurrencies derive security and validity from cryptographic algorithms and network consensus. This foundational distinction produces the varying advantages each system offers.

Advantages of Fiat Currency

Stability and Regulatory Protection

Fiat currencies offer unparalleled stability compared to the volatile cryptocurrency markets. The U.S. dollar, for instance, has maintained relatively consistent purchasing power over decades, with the Federal Reserve actively managing monetary policy to control inflation and stabilize the economy. According to the Bureau of Labor Statistics, the U.S. inflation rate has averaged approximately 2-3% annually in recent years, providing predictable economic conditions for planning and transactions.

— Bitnomial (@Bitnomial) October 8, 2025

Government-backed financial systems provide robust consumer protections that cryptocurrencies currently cannot match. The Federal Deposit Insurance Corporation (FDIC) insures bank deposits up to $250,000 per depositor, protecting consumers from bank failures. Credit card companies offer fraud protection, and regulatory frameworks exist to resolve disputes between parties. The Consumer Financial Protection Bureau (CFPB) handles complaints and enforces protections that simply don’t exist in most cryptocurrency transactions.

Universal Acceptance and Infrastructure

Fiat currencies benefit from centuries of infrastructure development. Every business worldwide accepts major fiat currencies, from local grocery stores to international corporations. This universal acceptance eliminates the friction of currency conversion and ensures that fiat money remains functional for daily transactions everywhere.

The existing financial infrastructure—ATMs, point-of-sale systems, wire transfer networks, and banking apps—represents trillions of dollars in investment that supports seamless monetary operations. Cryptocurrency adoption, while growing rapidly, still requires specialized knowledge and often involves additional steps for everyday purchases.

Inflation Management Tools

Central banks possess powerful tools to manage inflation and economic downturns that cryptocurrency systems cannot replicate. Through monetary policy mechanisms like interest rate adjustments, open market operations, and quantitative easing, central banks can respond to economic crises in ways that decentralized cryptocurrencies cannot. During the 2008 financial crisis and the COVID-19 pandemic, central banks deployed unprecedented stimulus measures that helped stabilize economies—actions that would be impossible within a fixed-cryptocurrency monetary system.

Advantages of Cryptocurrency

Decentralization and Transparency

Perhaps the most significant advantage cryptocurrency offers is true decentralization. No single government, bank, or corporation controls the money supply or transaction validation. Bitcoin’s network, for example, operates across thousands of nodes worldwide, making it theoretically immune to government shutdown or manipulation.

Blockchain technology provides unprecedented transparency. Every transaction is recorded on a public ledger that anyone can inspect. This transparency reduces opportunities for corruption, money laundering, and fraud in ways traditional financial systems struggle to match. Organizations like the World Bank and various governments have begun exploring blockchain for aid distribution and voting systems precisely because of this transparency guarantee.

Lower Transaction Costs and Speed

Cross-border cryptocurrency transactions typically cost a fraction of traditional wire transfers or international payment services. According to a 2023 World Bank report, average remittance costs globally hover around 6-7% of the transaction amount, while cryptocurrency transfers often cost less than 1% regardless of distance. For international businesses processing millions in transactions, these savings compound significantly.

Transaction speed represents another major advantage. Traditional international wire transfers can take 3-5 business days to settle. Cryptocurrency transactions typically confirm within minutes to hours, with newer blockchain networks achieving near-instant finality. This speed proves particularly valuable for time-sensitive business operations and humanitarian aid distribution where traditional banking delays could have serious consequences.

Financial Inclusion Potential

Approximately 1.4 billion adults globally lack access to traditional banking services, according to the World Bank’s 2023 Global Findex Database. Cryptocurrency offers these unbanked populations a pathway to participate in the global economy. All that’s required is a smartphone and internet connection—no physical bank branches, identification documents, or minimum balances necessary.

This financial inclusion potential has attracted attention from organizations like the United Nations, which has explored cryptocurrency as a tool for delivering aid to regions where traditional banking infrastructure is nonexistent or unreliable. Projects in Kenya, Nigeria, and the Philippines have demonstrated promising results for cryptocurrency-based financial inclusion initiatives.

Programmable Money and Smart Contracts

Cryptocurrency enables programmable money through smart contracts—self-executing agreements with terms directly written into code. These programs automatically enforce and execute contract conditions when predetermined criteria are met, eliminating the need for intermediaries like lawyers, notaries, or escrow services.

Ethereum, the second-largest cryptocurrency by market capitalization, was specifically designed to support these capabilities. Smart contracts can automate complex financial arrangements including insurance claims processing, supply chain verification, and decentralized finance (DeFi) applications like lending protocols and yield farming. This programmable capability represents a fundamentally new approach to financial agreements that fiat currency systems cannot replicate.

Comparative Analysis: When Each Excels

Understanding when to use cryptocurrency versus fiat money requires examining specific use cases and contexts.

For everyday purchases and bill payments, fiat currency remains superior due to universal acceptance, stable purchasing power, and robust consumer protections. Walking into any store and paying with dollars requires no technical knowledge, no internet connection, and offers immediate finality.

For international business transactions, cryptocurrency often provides advantages through lower fees, faster settlement, and reduced currency conversion complications. Companies like Microsoft, AT&T, and Overstock have accepted cryptocurrency for years, recognizing these benefits for certain transaction types.

For investment and wealth preservation, the choice becomes more nuanced. Gold has served as a traditional hedge against inflation for millennia, and some investors view Bitcoin as “digital gold” with similar properties. However, cryptocurrency’s extreme volatility—Bitcoin has experienced single-day drops exceeding 30%—makes it unsuitable for conservative investors or those needing predictable value storage.

For individuals in unstable economies, cryptocurrency offers escape routes from hyperinflation and capital controls. Citizens of countries like Venezuela, Argentina, and Lebanon have increasingly turned to cryptocurrency to preserve wealth when local currencies collapse. In these scenarios, cryptocurrency’s decentralized nature provides protection unavailable through traditional banking.

Expert Perspectives on the Future

Financial experts remain divided on cryptocurrency’s long-term role in the global economy.

J.P. Morgan analysts have acknowledged blockchain technology’s potential while maintaining that digital currencies will complement rather than replace traditional money. Their research indicates that central bank digital currencies (CBDCs)—government-issued digital currencies using blockchain technology—may represent the most likely evolution of digital money.

Conversely, proponents like Michael Saylor, CEO of MicroStrategy, argue that Bitcoin will eventually serve as the primary store of value for institutions, displacing gold’s historical role. Saylor’s company has invested billions in Bitcoin, positioning it as “digital property” rather than currency.

The International Monetary Fund (IMF) has taken a cautious approach, recognizing cryptocurrency’s efficiency benefits while emphasizing risks including financial stability concerns, environmental impact, and potential for illicit activities. Their 2023 report suggested that “appropriate regulatory frameworks” rather than outright bans would best balance innovation with consumer protection.

Implementation Considerations

For those interested in incorporating cryptocurrency into their financial activities, several practical considerations apply.

Security infrastructure demands serious attention. Unlike bank accounts protected by FDIC insurance, cryptocurrency holdings require personal responsibility for security. Hardware wallets—physical devices that store cryptocurrency keys offline—represent the gold standard for security. Software wallets offer convenience but present larger attack surfaces.

Tax implications in the United States treat cryptocurrency as property for federal tax purposes. The IRS requires reporting cryptocurrency transactions, and failure to do so can result in penalties. Before engaging with cryptocurrency, consulting a tax professional familiar with digital assets proves advisable.

Regulatory monitoring remains essential as governments worldwide develop cryptocurrency regulations. The regulatory landscape continues evolving rapidly, with different jurisdictions implementing varying approaches that can significantly impact cryptocurrency users.

The Complementary Future

Rather than a binary choice between cryptocurrency and fiat money, the most likely future involves both systems coexisting and potentially converging. Central banks worldwide are exploring CBDCs—digital versions of their fiat currencies that incorporate blockchain technology’s benefits while maintaining governmental control.

This hybrid future would allow individuals to choose between traditional banking, cryptocurrency, or CBDCs based on specific needs—using fiat for stable transactions, cryptocurrency for international transfers or investment, and CBDCs for government-issued digital payments.

Frequently Asked Questions

Is cryptocurrency better than fiat money for everyday purchases?

For everyday purchases, fiat money remains superior due to universal acceptance, stable value, and consumer protections. Cryptocurrency adoption for retail transactions requires merchants to accept it, special software or hardware wallets, and exposes users to significant price volatility during the transaction period.

Can cryptocurrency replace traditional banks?

Cryptocurrency can replace some banking functions like money transfers and basic storage, but traditional banks provide essential services including loans, interest payments, regulatory protections, and financial advice that decentralized systems cannot easily replicate. A hybrid model seems more likely than complete replacement.

Which is more secure: cryptocurrency or fiat money?

Security depends on context. Fiat money in insured bank accounts offers protection against loss through regulatory mechanisms. Cryptocurrency offers security against censorship and government seizure but exposes users to permanent loss if private keys are forgotten or stolen. Both systems have vulnerabilities but in different areas.

How do transaction fees compare between cryptocurrency and fiat money?

Cryptocurrency transactions typically cost $0.50-$5 regardless of amount, while traditional wire transfers and credit card processing often charge 1-3% plus flat fees. For large international transfers, cryptocurrency can save significantly in fees. For small domestic purchases, traditional methods often work fine with minimal visible fees built into prices.

Is investing in cryptocurrency safer than keeping money in savings accounts?

This depends entirely on individual risk tolerance. Savings accounts offer near-zero risk but also near-zero real returns after inflation. Cryptocurrency offers potential high returns but carries extreme volatility and the possibility of total loss. Financial advisors generally recommend cryptocurrency only as a small portion of diversified portfolios for those who can afford to lose the investment.

Are cryptocurrency transactions truly anonymous?

Most cryptocurrencies are pseudonymous rather than anonymous. Transactions are publicly visible on the blockchain, and law enforcement has developed sophisticated tools to trace transactions and identify users. Privacy-focused cryptocurrencies like Monero offer stronger anonymity, but even these face increasing regulatory scrutiny.