Blockchain technology has evolved from a niche concept behind cryptocurrency to a transformative force reshaping industries from finance to healthcare. At its core, blockchain is a distributed ledger that records transactions across many computers in a way that makes the records extremely difficult to alter retroactively. This fundamental characteristic—immutability combined with decentralization—creates trust between parties who may have no reason to trust each other otherwise.

This guide breaks down blockchain technology into plain English, explaining how it works, why it matters, and what it means for your digital future.

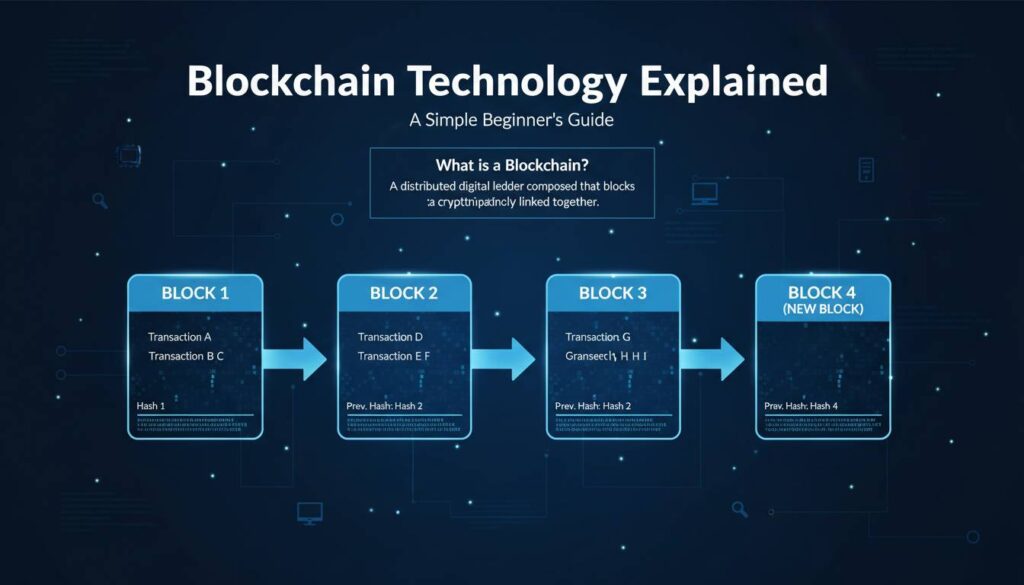

What Exactly Is Blockchain?

A blockchain is a digital database or ledger that is distributed across a network of computers. The term “blockchain” comes from how the technology stores data: information is grouped into “blocks” that are then “chained” together chronologically. Each block contains three key elements: data, a cryptographic hash (a unique digital fingerprint), and the hash of the previous block.

— paulbramas.eth (@BramasPaul) April 4, 2025

The simplest way to understand blockchain is to imagine a shared Google Document that everyone with access can read, but no one can delete or change what’s already written. Once something is recorded, it’s there permanently. This eliminates the need for intermediaries like banks or notaries because the system itself guarantees accuracy and honesty.

The technology was first introduced in 2008 when an unknown person or group using the name Satoshi Nakamoto published a whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This paper proposed using blockchain to create a digital currency that could be transferred directly between people without a bank. The first Bitcoin block, called the Genesis Block, was mined in January 2009, marking the real-world birth of blockchain technology.

How Blockchain Works: The Technical Foundation

Understanding blockchain requires understanding four key mechanisms that work together to create a secure, trustless system.

You want to understand how the Blockchain works? Watch this great explanation by Anders Brownworth https://t.co/nr4F3uJAHJ

— Globe (@globe) June 30, 2021

Blocks and Hashing

Every transaction on a blockchain gets bundled into a block. Each block contains three components: the data (transaction details), a hash (a 64-character alphanumeric string generated by a mathematical algorithm), and the previous block’s hash. When any information in a block changes, the hash changes completely—this is critical for security because it immediately invalidates the block.

Checkpoint Day :

Today I reviewed my learnings and made some notes AND came across this gem 👉 https://t.co/5QB79VcwSs

Probably the clearest visual explanation of cryptocurrency I’ve seen, absolute gold for beginners.#DevLog #WebDev #Blockchain #30DaysOfCode— Abhay Kumar Sahu (@abhayk_01) September 8, 2025

The hashing process uses complex mathematical functions that convert any input into a fixed-length output. For example, the hash of the word “hello” looks completely different from “hello1,” making it impossible to reverse-engineer the original data from the hash. This one-way function ensures that once data is recorded, it cannot be modified without detection.

The Chain Structure

Blocks link together sequentially using hashes, forming an immutable chain. If someone tries to tamper with a block from the past, its hash changes, breaking the link to the next block. The attacker would need to recalculate every subsequent block to make the chain valid again—which becomes computationally impossible as the chain grows longer.

If you're curious about Blockchain – what is it and how it works – a nice, clear, high-level overview is just what you need.

So check out this article by @ZubinPratap and learn the basics of Blockchain explained in plain English.https://t.co/tlDLISkrfa

— freeCodeCamp.org (@freeCodeCamp) February 11, 2020

This structure means that the more blocks that exist after a particular transaction, the more secure it becomes. Altering historical records becomes exponentially difficult, making older transactions virtually permanent.

Consensus Mechanisms

Blockchains need a way for distributed computers (nodes) to agree on which transactions are valid. This is called “consensus,” and two main mechanisms exist:

Proof of Work (PoW) requires computers (miners) to solve complex mathematical puzzles to add new blocks. This process consumes significant energy but provides strong security. Bitcoin uses PoW, and as of 2024, the Bitcoin network consumes more electricity annually than some countries like Norway or Argentina.

Proof of Stake (Stakeholders) requires validators to lock up (“stake”) their cryptocurrency as collateral to propose new blocks. If they validate fraudulent transactions, they lose their stake. Ethereum transitioned to Proof of Stake in 2022, reducing its energy consumption by approximately 99.95%.

Decentralization

Unlike traditional databases stored on single servers, blockchain copies exist across thousands of computers worldwide. No single entity controls the network, and no single point of failure exists. If one computer goes offline, the blockchain continues operating because thousands of other copies remain intact.

This decentralization is what makes blockchain fundamentally different from existing database technologies—and why it has the potential to disrupt industries beyond cryptocurrency.

Why Blockchain Matters: Key Advantages

Blockchain offers several distinct advantages over traditional record-keeping systems, making it valuable for applications far beyond digital money.

| Advantage | Traditional Systems | Blockchain |

|---|---|---|

| Trust | Requires intermediaries (banks, lawyers) | Trustless—code enforces rules |

| Transparency | Limited visibility, siloed data | Public, auditable transactions |

| Immutability | Records can be altered or deleted | Once recorded, virtually permanent |

| Speed | Days or weeks for cross-border transfers | Minutes to hours |

| Cost | High fees for intermediaries | Lower transaction costs |

| Security | Single point of failure | Distributed, cryptographic security |

Immutability and Auditability

Once data enters a blockchain, it cannot be changed without detection. This creates an immutable audit trail that organizations can use to prove exactly what happened and when. For supply chains, this means tracking products from origin to consumer with absolute certainty. For voting systems, it means eliminating questions about ballot tampering.

Reduced Intermediaries

Traditional transactions require trusted intermediaries—banks verify funds, notaries verify identities, lawyers verify contracts. Blockchain eliminates these middlemen through smart contracts: self-executing programs that automatically enforce agreement terms when conditions are met. According to a 2023 IBM study, blockchain-based smart contracts can reduce business contract costs by up to 75%.

Enhanced Security

Blockchain uses advanced cryptography—the same technology that protects military communications and financial systems. Each transaction requires cryptographic signatures, and the distributed nature means there’s no single vulnerability point. Hackers would need to simultaneously compromise thousands of computers to alter the record.

Real-World Applications Beyond Cryptocurrency

While cryptocurrency remains blockchain’s most famous application, the technology is transforming numerous industries.

Supply Chain Management

Walmart uses blockchain to track leafy greens from farm to store, reducing the time to trace food origins from 7 days to 2.2 seconds. Similarly, De Beers traces diamonds from mine to retail, ensuring conflict-free stones reach consumers.

Healthcare

Medical records on blockchain improve patient data portability while maintaining privacy. Patients control who accesses their records, and healthcare providers can verify credentials instantly. IBM and Mayo Clinic are among organizations piloting blockchain health record systems.

Financial Services

Beyond cryptocurrency, banks use blockchain for cross-border payments, trade finance, and identity verification. JPMorgan’s Onyx platform processes over $1 billion in daily transactions using blockchain technology.

Real Estate

Property records on blockchain reduce fraud, speed transactions, and eliminate the need for title companies. Countries like Georgia, Sweden, and Ukraine have piloted blockchain land registry systems.

Voting

Blockchain voting systems create tamper-proof election records. West Virginia successfully tested blockchain voting for military personnel overseas in 2018, and several countries are exploring similar systems.

Types of Blockchains: Public vs. Private

Not all blockchains operate the same way. Understanding the differences helps explain why certain use cases suit specific blockchain types.

| Type | Description | Examples | Best For |

|---|---|---|---|

| Public | Anyone can join, read, write, validate | Bitcoin, Ethereum | Decentralized apps, DeFi |

| Private | Invitation-only, controlled access | Hyperledger Fabric | Enterprise solutions |

| Consortium | Multiple organizations govern | R3 Corda | Banking, supply chains |

Public blockchains offer maximum decentralization and censorship resistance but sacrifice speed and privacy. Private blockchains offer speed and privacy but sacrifice decentralization. Consortium blockchains balance these tradeoffs by letting multiple organizations share control.

Common Misconceptions About Blockchain

Several myths surround blockchain technology that deserve clarification.

“Blockchain is the same as cryptocurrency” — False. Cryptocurrency is one application of blockchain. Blockchain is the underlying technology; cryptocurrency is just one use case.

“Blockchain is completely anonymous” — Partially false. Most blockchains are pseudonymous, not anonymous. Transactions link to public addresses, and with enough analysis, identities can sometimes be revealed. Privacy-focused blockchains like Monero and Zcash offer stronger anonymity.

“Blockchain can’t be hacked” — False. Individual blockchain projects get hacked, especially smart contracts with coding vulnerabilities. The 2022 Ronin Bridge hack resulted in $625 million in losses. Blockchain’s security comes from decentralization, not invulnerability.

“Blockchain is only for criminals” — False. While early cryptocurrency adoption had illicit use cases (the Silk Road marketplace), legitimate blockchain adoption now vastly outweighs criminal use. Chainalysis data shows criminal transactions represent less than 0.5% of crypto transaction volume.

The Challenges and Limitations

Blockchain isn’t a perfect solution. Understanding its limitations prevents unrealistic expectations.

Scalability

Public blockchains face throughput limits. Bitcoin processes about 7 transactions per second; Visa processes about 24,000. While layer-2 solutions and blockchain upgrades address this, scalability remains an active challenge.

Energy Consumption

Proof of Work blockchains consume substantial energy. Bitcoin’s annual energy consumption rivals some small countries. While Proof of Stake reduces this dramatically, environmental concerns persist.

Regulatory Uncertainty

Governments worldwide are still determining how to regulate blockchain. Some countries embrace it; others restrict or ban cryptocurrency. This uncertainty creates challenges for businesses building blockchain solutions.

User Experience

Managing private keys, understanding gas fees, and navigating wallet security create barriers for average users. If blockchain goes mainstream, user experience must improve substantially.

The Future of Blockchain Technology

Blockchain continues evolving rapidly, with several trends shaping its future.

Interoperability allows different blockchains to communicate, enabling cross-chain applications and reducing fragmentation. Projects like Polkadot and Cosmos facilitate this connectivity.

Web3 represents the vision of a decentralized internet where users own their data and digital assets. Blockchain serves as its foundation, enabling ownership, identity, and value transfer without traditional intermediaries.

Central Bank Digital Currencies (CBDCs) use blockchain technology for government-issued digital currency. Over 130 countries, representing 98% of global GDP, are exploring or piloting CBDCs.

Enterprise adoption continues accelerating, with major corporations investing in blockchain infrastructure. According to Gartner, blockchain is projected to generate $3 trillion in commercial value by 2030.

Frequently Asked Questions

What is blockchain in simple terms?

Blockchain is a digital ledger that records information across many computers simultaneously. Once information is recorded, it’s extremely difficult to change. Think of it as a shared, permanent document that thousands of people can see but no one can secretly modify.

How is blockchain different from a regular database?

Traditional databases are controlled by single entities (companies or organizations) and can be edited or deleted by administrators. Blockchain is decentralized—no single party controls it—and information cannot be altered once recorded. This creates trust without requiring a central authority.

Is blockchain only for cryptocurrency?

No. While cryptocurrency was blockchain’s first major application, the technology now serves many industries including supply chain management, healthcare, real estate, voting systems, and financial services. Any situation requiring trusted record-keeping can benefit from blockchain.

Can blockchain be hacked?

While blockchain itself is highly secure due to its distributed nature and cryptographic protection, individual blockchain projects and applications can be vulnerable. Smart contract bugs, phishing attacks, and centralized exchange breaches have resulted in significant losses. Security depends on implementation quality, not just the underlying technology.

How do I get started with blockchain?

Start by understanding the basics: download a cryptocurrency wallet (like Coinbase Wallet or MetaMask), explore blockchain explorers (like Etherscan for Ethereum), and try small transactions to understand how it works. Many educational resources exist, including courses from platforms like Coursera and edX.

Will blockchain replace banks?

Not entirely, but it will change financial services significantly. Blockchain enables faster, cheaper cross-border payments and new financial products like decentralized finance (DeFi). Some banking functions may become unnecessary, but banks are also adopting blockchain technology to improve their own services.