Decentralized Finance (DeFi) represents a fundamental restructuring of traditional financial systems, replacing intermediaries like banks and brokerage firms with permissionless, blockchain-based protocols that enable peer-to-peer financial transactions. In 2024, the DeFi ecosystem holds over $80 billion in total value locked (TVL), reflecting a technology movement that challenges century-old financial infrastructure while creating new opportunities for millions of users worldwide.

Key Insights

– DeFi eliminates intermediaries by using smart contracts to execute financial agreements automatically

– The total value locked in DeFi protocols reached $80 billion in early 2024, recovering from 2022’s market correction

– Major DeFi platforms process billions in daily trading volume through decentralized exchanges

– Yield farming and liquidity provision have created new income streams for crypto holders

– Regulatory scrutiny is increasing as traditional financial institutions engage with DeFi protocols

What is DeFi? Understanding the Basics

DeFi refers to a collection of financial applications built on public blockchains—primarily Ethereum—that replicate traditional financial instruments without relying on centralized intermediaries. These applications use smart contracts, which are self-executing programs stored on the blockchain that automatically enforce the terms of an agreement when predetermined conditions are met.

https://twitter.com/thedefiedge/status/1874813658892767292

The fundamental difference between traditional finance and DeFi lies in the removal of trust in a central authority. In conventional banking, you trust that a bank will hold your funds, process your transactions correctly, and provide you with interest on deposits. DeFi replaces this trust in an institution with trust in code—specifically, in the transparent, auditable smart contracts that govern financial interactions.

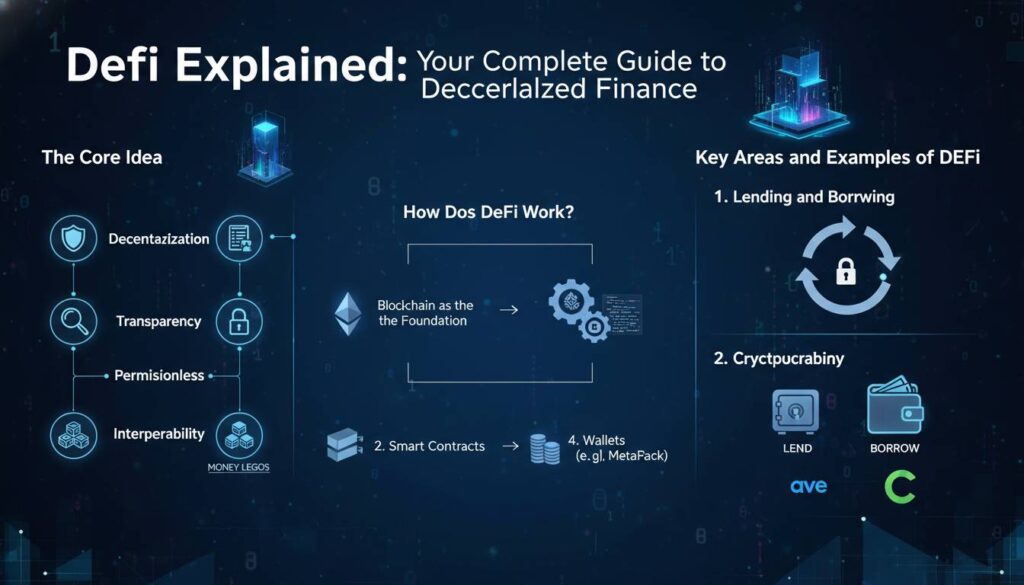

Core Principles of Decentralized Finance

Permissionless Access: Anyone with an internet connection and a cryptocurrency wallet can access DeFi protocols. Unlike traditional finance, which requires identity verification, credit checks, and approval processes, DeFi is open by default. This accessibility has proven particularly significant in regions where banking services remain limited.

Transparency: All transactions and smart contract code on public blockchains are publicly verifiable. Users can examine the underlying code of any DeFi protocol to understand exactly how their funds will be handled. This represents a dramatic shift from traditional finance, where internal operations remain opaque to customers.

Interoperability: DeFi protocols are designed to work together like financial building blocks. You can deposit tokens into one protocol, use those tokens as collateral in another, and invest the proceeds in yet another—all without leaving the blockchain ecosystem.

Programmable Money: Unlike traditional currencies and financial instruments, DeFi tokens and assets can be programmed with specific rules. Interest rates can adjust automatically based on market conditions, collateral can be liquidated instantly when values drop, and complex financial products can be created through combinations of existing protocols.

How DeFi Works: The Technical Foundation

Understanding DeFi requires grasping how smart contracts enable financial functions that traditionally required institutional intermediaries. These self-executing agreements form the backbone of every DeFi application.

Has anyone seen DeFi mechanics applied to knowledge platforms rather than financial assets?

byu/coobook indefi

Smart Contracts as Financial Infrastructure

A smart contract is code deployed to a blockchain that automatically executes when specific conditions are met. Consider a simple savings account: in traditional finance, you deposit money, the bank credits your account with interest, and you withdraw funds later. In DeFi, this process transforms into a smart contract that accepts your deposit, calculates interest every second based on an algorithm, and allows withdrawal at any time—without any bank employee ever touching your funds.

This programmability enables what developers call “composability”—the ability to combine multiple smart contracts to create new financial products. A developer can take a lending protocol, add a stablecoin wrapper, layer on an insurance contract, and create an entirely new financial instrument within hours.

The Role of Oracles

Smart contracts cannot access data outside the blockchain on their own. This limitation presents a challenge: how does a lending protocol know what the current price of Ethereum is to determine if a loan should be liquidated?

Oracle networks solve this problem by feeding external data into the blockchain. Services like Chainlink aggregate price data from numerous centralized exchanges and deliver it to DeFi protocols in a reliable, tamper-proof manner. When you borrow against your crypto holdings, the oracle tells the protocol whether your collateral remains sufficient.

Liquidity Pools and Automated Market Makers

Traditional stock exchanges rely on order books—lists of buy and sell orders waiting to be matched. DeFi largely replaced this model with liquidity pools, which are smart contracts containing reserves of two tokens. When you want to trade, you swap directly with the pool rather than waiting for another user to match your order.

Automated Market Makers (AMMs) use mathematical formulas to determine token prices based on the ratio of tokens in the pool. The most common formula, used by Uniswap, maintains constant product pricing where the product of the quantities of both tokens remains constant regardless of trade size. This mechanism ensures the pool always has liquidity but causes price slippage—the larger your trade, the worse the price you receive.

Key DeFi Use Cases and Applications

The DeFi ecosystem has expanded far beyond simple token swaps. Today, users can lend, borrow, earn interest, insure against smart contract failures, trade with leverage, and access synthetic assets that track real-world commodities.

Decentralized Lending and Borrowing

Platforms like Aave, Compound, and MakerDAO enable users to lend their crypto assets and earn interest or borrow against their holdings without credit checks or identity verification. The interest rates adjust algorithmically based on supply and demand—more borrowers mean higher rates for lenders.

This system has created significant opportunities for crypto holders who want to put their assets to work without selling them. You can deposit your Ethereum, earn a yield while retaining exposure to any future price appreciation, and still use that deposited ETH as collateral for a loan.

Notable Platforms:

– Aave: One of the largest DeFi lending protocols, supporting over 20 different collateral types and offering both stable and variable interest rates

– Compound: A pioneer in algorithmic interest rates that has facilitated over $20 billion in cumulative borrowing

– MakerDAO: The protocol behind DAI, a decentralized stablecoin soft-pegged to the US Dollar

Decentralized Exchanges

DEXs like Uniswap, Curve, and SushiSwap facilitate token trading directly from users’ wallets. Unlike centralized exchanges that hold user funds, DEXs use liquidity pools, meaning users trade against funds provided by other participants.

Uniswap, launched in 2018, has become the most popular DEX, processing billions in daily trading volume. Its V3 iteration introduced concentrated liquidity, allowing liquidity providers to concentrate their funds within specific price ranges to maximize efficiency.

Stablecoins

DeFi depends heavily on stablecoins—cryptocurrencies designed to maintain a fixed value, typically $1. These tokens enable traders to exit volatile positions without leaving the crypto ecosystem and serve as the primary medium of exchange within DeFi protocols.

The largest stablecoins include:

– USDT (Tether): The largest by market capitalization, though subject to ongoing controversy regarding reserves

– USDC: A regulated stablecoin backed by fully reserved assets, widely accepted in DeFi

– DAI: A decentralized stablecoin created by MakerDAO, over-collateralized by crypto assets rather than fiat

Yield Farming and Staking

Yield farming involves moving tokens between different DeFi protocols to maximize returns. A yield farmer might deposit tokens in a lending protocol to earn interest, then take the received tokens and deposit them in a different protocol that rewards users with its own governance token.

Staking, particularly relevant after Ethereum’s transition to Proof of Stake in 2022, involves locking up cryptocurrency to support network operations and earning rewards in return. DeFi staking often refers to locking tokens in protocols to earn additional tokens as incentives.

Major DeFi Protocols and Platforms

The DeFi landscape features numerous protocols competing for user adoption and total value locked. Understanding the major players helps contextualize the ecosystem’s structure.

| Protocol | Category | TVL (Approx.) | Key Feature |

|---|---|---|---|

| MakerDAO | Lending/Stablecoin | $7B+ | DAI stablecoin creation |

| Aave | Lending | $10B+ | Variable rate lending |

| Uniswap | Exchange | $4B+ | Largest DEX by volume |

| Curve | Exchange | $2B+ | Stablecoin trading |

| Compound | Lending | $1B+ | Algorithmic interest rates |

| Lido | Staking | $15B+ | Liquid staking (ETH) |

MakerDAO, created by Rune Christensen in 2017, remains foundational to DeFi as the creator of DAI, the first decentralized stablecoin. The protocol requires users to lock collateral—initially ETH, later multiple assets—to generate DAI loans. This over-collateralization model has proven remarkably resilient, maintaining DAI’s peg even during extreme market volatility.

Aave, originally called ETHLend before rebranding, pioneered flash loans—uncollateralized loans that must be repaid within a single blockchain transaction. This seemingly impossible financial instrument demonstrates smart contracts’ ability to create entirely new financial products impossible in traditional finance.

Risks and Challenges in Decentralized Finance

DeFi’s promise of open, transparent financial infrastructure comes with significant risks that users must understand before participating.

Smart Contract Risk

Smart contracts contain code, and code can contain bugs. Even audited protocols have experienced exploits that resulted in millions of dollars in losses. The Wormhole bridge hack in February 2022 saw approximately $320 million stolen due to a signature verification vulnerability. Users must accept that depositing funds into any smart contract carries the risk of complete loss if a vulnerability is exploited.

Impermanent Loss

Liquidity providers on AMMs face a unique risk called impermanent loss. When you deposit tokens into a liquidity pool and those tokens’ prices change relative to each other, you may end up with less value than if you had simply held the tokens. This loss becomes permanent when you withdraw, unlike the temporary state that gives it its name.

Regulatory Uncertainty

DeFi exists in a legal gray area worldwide. Regulators increasingly focus on decentralized protocols, with the U.S. Securities and Exchange Commission has pursued enforcement actions against several DeFi projects. The question of how to regulate code that operates without a central party remains largely unanswered.

Counterparty and Platform Risk

While DeFi removes traditional financial intermediaries, it introduces new ones—protocol developers, oracle providers, and governance token holders who may make decisions affecting users. Protocols can change parameters, upgrade code, or in extreme cases, be captured by malicious actors.

The Future of DeFi: Trends and Predictions

The DeFi ecosystem continues evolving rapidly, with several trends shaping its future trajectory.

Institutional participation increased significantly in 2023-2024, with major financial firms exploring DeFi for treasury management and cross-border payments. BlackRock’s tokenized fund initiative represents one of the most significant traditional finance entries into blockchain-based financial infrastructure.

Layer-2 scaling solutions, particularly Arbitrum and Optimism, have reduced transaction costs while maintaining security, making DeFi more accessible for smaller participants. These rollup technologies batch transactions off-chain while publishing compressed data to Ethereum, dramatically improving throughput.

The emergence of real-world asset tokenization represents another significant trend. Protocols are bringing traditional assets—real estate, treasury bills, commodities—onto-chain, potentially expanding DeFi’s utility beyond purely crypto-native use cases.

Regulatory frameworks will likely crystallize over the coming years, potentially requiring DeFi protocols to implement compliance measures or creating compliant alternatives that maintain DeFi’s accessibility principles.

Frequently Asked Questions

What is the difference between DeFi and traditional finance?

DeFi replaces centralized intermediaries like banks and brokerages with blockchain-based smart contracts that execute financial transactions automatically. Traditional finance relies on trusted institutions to hold funds, process transactions, and enforce agreements, while DeFi relies on publicly verifiable code. DeFi offers 24/7 access, permissionless participation, and programmable financial products, but lacks the consumer protections and established regulatory frameworks of traditional finance.

How do I start using DeFi?

To begin using DeFi, you need a cryptocurrency wallet like MetaMask or Rabby, some cryptocurrency (typically Ethereum or tokens on Ethereum-compatible networks), and a small amount of ETH to pay for network transaction fees. Start by connecting your wallet to a decentralized exchange like Uniswap to swap tokens, then explore lending protocols like Aave or Compound to earn interest. Begin with small amounts to understand how transactions work before committing significant funds.

Is DeFi safe to use?

DeFi carries substantial risks including smart contract vulnerabilities, potential loss of funds through hacks or exploits, and total loss of access if you lose your wallet seed phrase. No DeFi platform offers the same consumer protections as traditional financial institutions. Users should only invest what they can afford to lose, use hardware wallets for significant holdings, and thoroughly research protocols before depositing funds.

What are gas fees in DeFi?

Gas fees are transaction costs paid to the blockchain network for processing your transaction. On Ethereum, these fees fluctuate based on network demand—during busy periods, simple transactions can cost $10-50 or more. Layer-2 networks like Arbitrum and Optimism offer significantly lower fees while maintaining Ethereum’s security. Users must account for gas costs when calculating whether DeFi activities are profitable.

Can I lose money in DeFi?

Yes, DeFi investments can lose value through multiple mechanisms: smart contract exploits that drain funds, impermanent loss from providing liquidity, token value decline, and platform failure. Unlike bank accounts, DeFi deposits are not insured by the FDIC. Many users have lost substantial amounts through protocol hacks or accidentally interacting with malicious contracts. The potential for high returns comes with correspondingly high risk.

Conclusion

DeFi represents a profound shift in how financial services are delivered, replacing trust in institutions with trust in transparent, auditable code. The ecosystem has grown from experimental projects to an infrastructure holding tens of billions in user funds, processing billions in daily transactions, and attracting attention from major traditional financial institutions.

For users willing to understand its risks, DeFi offers unprecedented access to financial services, new earning opportunities, and participation in the construction of alternative financial infrastructure. The technology remains in its early stages—security improves continuously, user interfaces become more intuitive, and regulatory frameworks gradually take shape.

The fundamental question for anyone considering DeFi is whether the promise of open, accessible, programmable finance outweighs the risks of an ecosystem still maturing. Those who choose to participate should approach with caution, start small, prioritize security practices, and recognize that they are using bleeding-edge financial technology that remains subject to significant volatility and uncertainty.